If you traded crypto in 2025, the IRS wants a detailed accounting of every transaction -- and that means filling out the right crypto tax form for each type of activity. Tax season hits different when you have gains buried across five exchanges, staking rewards, and that NFT flip from January you'd rather forget. The IRS isn't forgetting it. For the 2025 tax year, filing cryptocurrency correctly means knowing exactly which forms you need, how to fill them out, and what gets you in trouble if you skip a step.

With BTC sitting at $68,815 and the Fear and Greed Index at 10 (Extreme Fear), a lot of traders are looking at losses this year, not gains. That actually makes the paperwork more manageable -- but you still have to file. Here is what you need to know.

The core crypto tax form options for the 2025 tax year

Most crypto investors need three forms to file correctly. Understanding what each one does saves a lot of confusion at the end.

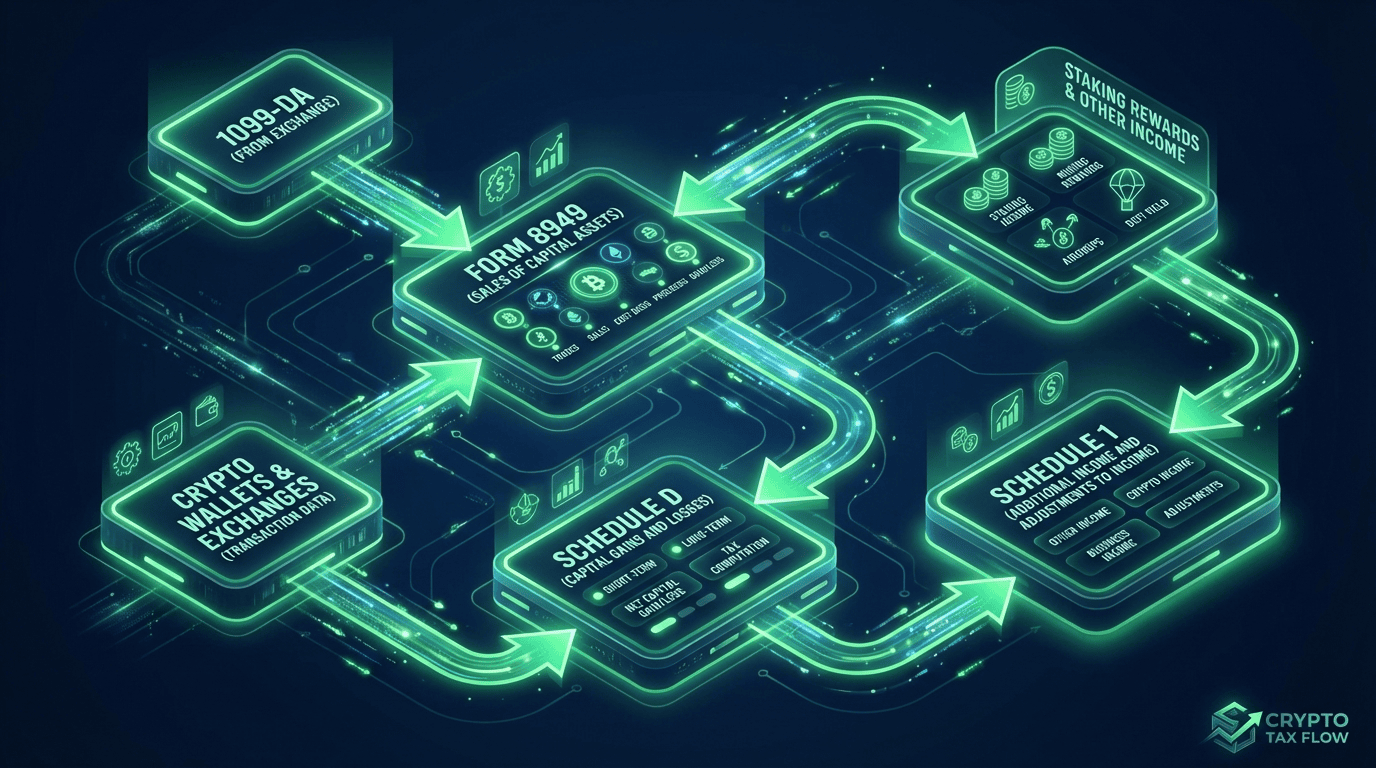

Form 8949 (Sales and Other Dispositions of Capital Assets) is where you list every single taxable crypto transaction: date acquired, date sold, proceeds, cost basis, and the resulting gain or loss. Every trade. Every sale. Every crypto-to-crypto swap. This is the detailed ledger the IRS wants.

Schedule D (Capital Gains and Losses) summarizes everything from Form 8949. Short-term gains (assets held under a year) go in one column, long-term gains (held over a year) in another. Schedule D is what the IRS uses to calculate your actual tax owed.

Schedule 1 (Additional Income and Adjustments) is where staking rewards, mining income, and airdrops land. These are treated as ordinary income -- not capital gains -- so they never touch Form 8949 or Schedule D. The IRS treats receiving crypto as payment for services the same way.

If you received a 1099-DA from your exchange, that form reports your gross proceeds to both you and the IRS. The 1099-DA is new for the 2025 tax year. Not every exchange is required to send one yet, but when you receive it, cross-reference it against your own records. The gross proceeds on the 1099-DA will rarely match your taxable gain because it doesn't account for your cost basis -- your job is to fill in that gap on Form 8949.

What counts as a taxable crypto event

This is where most people go wrong. The IRS does not care whether you received dollars at the end. If value changed hands involving crypto, it is almost certainly a taxable event.

These transactions trigger a tax event:

- Selling crypto for USD or any fiat currency

- Trading one cryptocurrency for another (BTC to ETH, for example)

- Using crypto to buy goods or services

- Receiving staking rewards, mining rewards, or interest from lending

- Getting an airdrop

- Earning yield through DeFi protocols

These do NOT trigger a tax event:

- Transferring crypto between your own wallets

- Buying crypto with USD (no disposition has occurred)

- Holding crypto without selling

One rule introduced for the 2025 tax year matters here: the IRS now requires wallet-by-wallet accounting for cost basis. You can no longer pool all your BTC holdings across exchanges and pick an average cost. Each wallet or exchange account is treated separately when calculating cost basis.

Trade Smarter While You File

Tax season is stressful. Your trading platform doesn't have to be. Join Bitunix and claim up to a $5,500 welcome bonus when you sign up.

Short-term vs long-term: the tax rate gap matters

How long you held before selling determines which tax rate applies. The difference is not small.

Short-term capital gains apply to assets held 365 days or less. These are taxed at your ordinary income rate -- the same bracket as your salary. Depending on your income, that can be anywhere from 10% to 37%.

Long-term capital gains apply to assets held more than 365 days. Rates are 0%, 15%, or 20% depending on your taxable income. Most middle-income filers pay 15%. This is why holding matters: the same gain that costs you 37% at short-term rates might cost you only 15% at long-term rates.

If you are sitting on losses this year -- which many crypto traders are -- you can use them to offset gains. If losses exceed gains, you can deduct up to $3,000 of net capital losses against ordinary income per year. Additional losses carry forward to future tax years. Our crypto tax calculator guide walks through the mechanics of loss harvesting in detail.

How to fill out Form 8949

Form 8949 has two parts. Part I covers short-term transactions, Part II covers long-term. The columns are the same in both:

- Column A: Description of the asset (e.g., "0.5 BTC")

- Column B: Date acquired

- Column C: Date sold or disposed

- Column D: Proceeds (what you received)

- Column E: Cost basis (what you paid, including fees)

- Column H: Gain or loss (Column D minus Column E)

Fees matter here. If you paid a $25 trading fee when buying BTC, that $25 adds to your cost basis. When you sell, the cost basis is higher, which means a smaller taxable gain. Don't ignore transaction fees -- they add up, especially if you trade frequently.

If you have more transactions than fit on one Form 8949, attach additional pages. Most crypto tax software handles this automatically, generating a completed Form 8949 you can attach to your return.

DeFi and staking: the messier part

DeFi introduced a layer of complexity the original tax forms were not designed for. The IRS has issued some guidance, but a lot of specific situations are still in a gray area.

Here is what the IRS has been clear about:

Staking rewards are taxable income when received. The fair market value of the tokens on the day you receive them is your income amount. That amount also becomes your cost basis when you eventually sell those tokens.

Liquidity pool tokens are treated as a taxable exchange when you deposit assets into a pool in exchange for LP tokens. You are disposing of your original assets and receiving new ones. When you withdraw, that is another taxable event.

Yield farming rewards are ordinary income, same as staking.

For most DeFi activity, you need a transaction history from your wallet. Tools like Koinly, TaxBit, or CoinLedger can pull on-chain data from wallets and format it for Form 8949. If you used DeFi heavily in 2025, this step is worth spending a few hours on before April.

For a broader look at tax strategy around DeFi specifically, see our crypto airdrop tax strategy guide which covers similar territory for airdrops.

How exchanges report to the IRS in 2025

The 1099-DA changed the reporting picture. Before 2025, crypto exchanges were not required to report individual transaction details to the IRS. Starting with the 2025 tax year, centralized exchanges operating in the US must report gross proceeds on Form 1099-DA.

What that means practically: the IRS now receives data directly from Coinbase, Kraken, and other US-regulated platforms. If you traded on those exchanges and don't report, there is now a paper trail. The IRS matching system will catch discrepancies.

One thing the 1099-DA does not include: your cost basis. The form shows what you sold for, not what you paid. That means even if you receive a 1099-DA, you still need to calculate your own cost basis and complete Form 8949 correctly. The 1099-DA is a check on your proceeds, not a replacement for your recordkeeping.

Exchanges outside the US are not covered by the 1099-DA requirement yet. But that doesn't mean those gains are exempt -- you still have to report them yourself.

Futures Trading With Up to $5,500 Bonus

Whether you're trading through a bear market or positioning for recovery, Bitunix gives you the tools to do it right. New users get up to $5,500 in welcome bonuses.

Getting your transaction history

The single biggest obstacle for most crypto filers is incomplete records. Here is how to get what you need.

Centralized exchanges: Log in, go to Account or Reports, and export your complete transaction history as a CSV for the full 2025 calendar year. Every major exchange has this feature. Do not use the mobile app for this -- the full export is usually only accessible on desktop.

DeFi wallets: Use a blockchain explorer like Etherscan for Ethereum transactions, or a dedicated tool like Koinly or CoinLedger that connects to your wallet address and pulls all on-chain activity automatically.

Cross-chain activity: If you bridged assets between chains (Ethereum to Solana, for example), you need records from both chains. Each bridge transaction may also be a taxable event depending on how it is structured.

Keeping a crypto trading journal throughout the year makes this a lot easier -- instead of reconstructing everything in March, you have a running record of every trade and its tax implications.

The most common crypto tax form filing mistakes

A few errors come up repeatedly when crypto investors file.

The biggest one: forgetting that crypto-to-crypto trades are taxable. If you swapped ETH for SOL in September, that is a taxable event. You disposed of ETH at its market value on the date of the trade, and that is the proceeds figure. Many people assume trades are only taxable when they "cash out" to dollars. The IRS does not agree.

Second most common: missing staking and interest income. If you earned yield on a lending platform or received staking rewards, that income goes on Schedule 1 regardless of whether the exchange sent you a 1099. Not receiving a form does not eliminate the tax obligation.

Third: incorrect cost basis method. With wallet-by-wallet accounting now required, the accounting method you choose (FIFO, HIFO, LIFO) applies per wallet, not across all holdings. HIFO (highest cost, first out) often produces the best tax result in a year with overall gains, but you need to apply it consistently within each wallet.

If you have significant crypto activity and are unsure, a tax professional who specializes in digital assets is worth the cost. The IRS has increased its enforcement around crypto, and the 1099-DA reporting requirement means the data is now flowing directly to them.

Our crypto tax rate guide covers exactly what brackets apply to your gains and how to calculate what you actually owe.

Key deadlines

Your 2025 tax return is due on April 15, 2026. If you need more time, you can file for an automatic six-month extension, which moves the deadline to October 15, 2026. The extension gives you more time to file, but not more time to pay -- if you owe taxes, interest and penalties accrue from April 15 regardless of when you file.

For most crypto investors dealing with losses at current prices, there is less urgency around the April deadline. But if you have gains from earlier in the cycle, sitting on an unpaid tax bill accrues interest daily. Better to file and pay on time.

If you are still sorting through your cost basis and genuinely can't file accurately by April 15, file the extension. Filing something incomplete is worse than filing late.